Paper trading has proven to be a valuable tool both for new and experienced traders to practice and test their strategies. By replicating to a great extent a real-life trading environment, users can validate their ideas without having to put any money at risk for doing so. Having said that, there are quite a few differences between paper trading platforms and real-life trading, which we will be covering extensively throughout this article.

There are both technical and psychological differences between paper trading and live trading. The main technical differences are the lack of information leakage, price slippage due to latency, the market impact of orders, and proper order queue positioning. Additionally, most simulators fail to account for dividend payments. When it comes to psychological aspects, paper trading oftentimes fails to replicate the risk aversion and loss aversion of traders.

Table of Contents

What is paper trading?

Paper trading, oftentimes also referred to as stock market simulators are platforms that enable users to place fictitious buy and sell orders as if they were in a real-life trading environment. It allows users to make their first steps in the financial industry without putting any money at risk. Additionally, experienced traders and algorithmic developers use paper trading as a means to validate their trading strategies.

Why is paper trading useful?

Whether you are a discretionary trader or a systematic algorithm developer, paper trading is an essential tool for testing the performance of a trading strategy. Even if you thoroughly backtested a strategy with historical prices, live trading it in a simulated environment with fake money can be very helpful for detecting possible pitfalls. Additionally, if you’re new to the financial markets, it is a good idea to get used to the inner workings of trading without risking any money.

It is not uncommon, even for experienced traders, to backtest a strategy without realizing that they introduced some sort of lookahead bias or overfitting into the strategy.

These problems lead to the strategy not performing as expected in the future since the parameters were fine-tuned to perform well in the past, but most probably only by replicating the noise in the data instead of finding consistent patterns. In order to avoid risking real money to find out if a strategy really generates alpha in a risk-adjusted way, paper trading is only logical to use.

Thus, a strategy that performs well both on backtests and on paper will have a greater probability of being profitable in real live trading.

Is paper trading the same as live trading?

Although paper trading is one of the best representations of a real live-trading environment, there are a few features and market microstructure considerations that most paper trading platforms fail to account for.

Additionally, there are also psychological differences between trading with real or fake money. Just to name a few, paper trading decreases the loss aversion of users and also fails to assess the risk of addiction.

Technical Differences between paper trading and live trading

Although paper trading platforms have improved their reliability and robustness when it comes to simulating a real training account, there are still a few differences that cannot be accounted for.

Most paper trading simulators fail to properly represent the impact on the market of our own orders, information leakage created when we place an order, order queue in which orders get filled, possible price improvements, regulatory fees, and dividend payments.

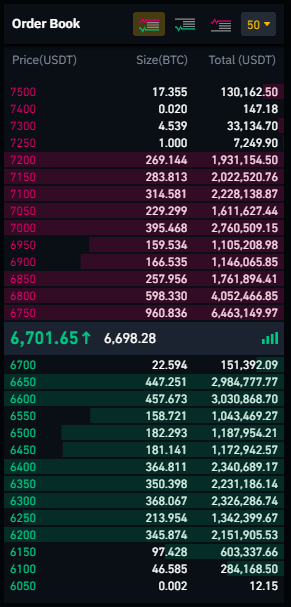

Market impact of your orders

Whenever you buy a place a market buy or sell order, you are buying at the lowest ask price and selling at the highest bid price. Additionally, if your placed order is of considerable size or if you’re trading an illiquid asset, your trade might have an impact on the order book and move the price.

Paper trading simulators can at the very best replicate the fill price you would have obtained if the trade were to be real, but cannot account for the impact on the price that it would have had. This is due to the fact that simulators are using real data, and as a consequence, the quoted prices only move as a consequence of real transactions.

Paper trading is thus a less reliable representation of reality if you’re simulating big orders or trading assets that have less volume traded.

Information leakage of your orders

When placing a limit buy or sell order, it gets added to the order book in its corresponding place. Due to the fact that everyone can see and analyze the live status of an order book, creating an order effectively leaks information regarding one’s own behavior into the market. Market makers and other high-frequency trading algorithms use this information in order to estimate the most probable next move in price.

On the other hand, simulated orders do not get added to the real order book, and thus they are not taken into account by high-frequency traders.

There are also cases in which a sudden increase in buying or selling an asset leads to market makers not participating anymore. This is because they assume that a news event is generating an order book imbalance and that it is trading with an information deficit. Therefore, if you were to place a considerable order on an illiquid asset, you would have a greater impact on the order book as expected, but paper order would fail to account for this impact.

Price slippage due to latency

When an algorithm trades on a higher frequency, latency becomes a relevant issue to account for. Say you’re receiving live data from a broker and one of your algorithms triggers a signal and sends an order to your broker. Unless the broker decides to fill the order internally, it will route it to an exchange.

Although this process is astoundingly fast, it still has a delay. Take Interactive Brokers as an example: they claim to have an order-acknowledgment latency of 75ms, and an order-to-trade delay of 130ms with the International Securities Exchange. Multiple trades would have been filled in those 130ms in the case of liquid assets during regular trading hours.

Given the fact that fictitious orders are not sent to the exchange and are “filled” internally by the simulator, the order-to-trade latency is eliminated. Although a more refined simulator could take implement an artificial delay in order to replicate the real latency, it would be an unnecessary feature for most traders.

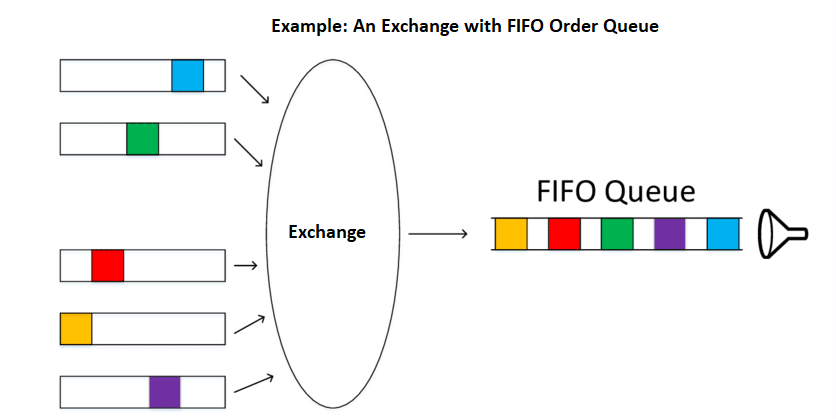

Order queue positioning

All exchanges fill orders by price priority, meaning that the highest bid and lowest ask are the first in line to be filled when a counterpart market order is routed to the exchange. Having said that, exchanges also have to define to queue priority of orders that have the exact same price. After queueing orders by their prices, the Chicago Mercantile Exchange (CME) queues in ascending order with regards to their timestamps (older orders have priority).

This distinction can be very important when simulating trading strategy, especially when it comes to market-making algorithms. If we were to create a very simple market-making algorithm that always places buy orders at the highest bid price and sell orders at the lowest ask price, said orders would by definition have always the least priority due to their timestamp. Paper trading simulators fail to account for time order queue position, and they would falsely fill the fictitious orders as if they were first in place.

Price improvement received

Although it depends on the paper trading platform you’re using, your orders are probably getting filled at the National Best Bid and Offer (NBBO) quotes, but there are some platforms that only use the quotes of a specific exchange.

Additionally, brokers are also allowed to fill the orders internally if they offer a higher bid or a lower ask. As a consequence, they use their own stock inventory and offer more competitive prices without ever routing the order to an exchange.

Paper trading simulators do not incorporate this feature as a possibility, since they could not estimate the price improvement in any reliable way.

Although this seems like an unimportant aspect to consider, it might be non-trivial for intraday trading algorithms. Make sure that your paper trading account has access to the same exchange as your real-life broker.

For example, the free data plan offered by Alpaca only provides access to IEX, which accounts for only 2.4% of the total volume traded in US markets. As a consequence, the bid-ask spread tends to be higher.

Dividends

Most paper trading simulators do not take into account dividend payments, and thus have a bias towards understating the true performance of portfolios that heavily rely on them. This is not only relevant when trading stocks, but also ETFs, since they pay out the full dividend that comes with holding the stocks that compose the ETF.

These issues are completely irrelevant when paper trading commodities or when testing intraday trading strategies with short holding periods. On the other hand, if you want to evaluate the performance of a portfolio comprised of a set of dividend-paying assets, make sure your simulator accounts for it.

Psychological differences between paper trading and live trading

In addition to technical differences between paper trading platforms and a real-life scenario, there are also psychological aspects that have to be considered when comparing them. The two most relevant have been studied thoroughly during the last decades in academia, and are none other than risk aversion and loss aversion.

Although addictive behavior is one of the differences, I won’t be covering the issue since I do not have any knowledge regarding mental health.

Risk Aversion

By this, we refer to the overall tendency of the population to prefer outcomes with low uncertainty over others with higher ones, even when they are identical on average. Thus, everyone’s risk profile could be imagined as a curve of risk-return, and the higher the risk, the higher the return they require to be willing to accept it. In short, this is why Argentinean bonds have higher interest rates than their US or Swiss counterparts.

When it comes to paper trading, the fact that the user is trading with fake money instead of his own savings leads to a distorted risk aversion profile. He might favor strategies with a higher risk profile instead of the ones he would be willing to use in a real-life scenario.

A clear example of a distorted risk aversion profile arises in college-level stock market competitions. Due to the nature of the competition, there’s no incentive to create a sound portfolio, but the game favors participants that create over-leveraged and highly risky strategies. Most of these participants will end up with 0 dollars on their paper accounts, but it’s almost certain that one of them will be the winner of the competition.

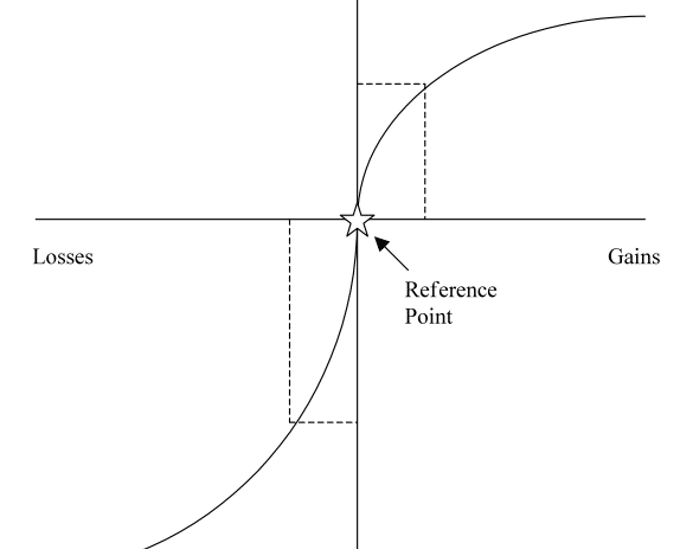

Loss Aversion

X-Axis: losses/gains

Y-Axis: perceived value/utility of those losses or gains

Source

This phenomenon has been studied and replicated multiple times in academia, it is especially applicable to financial markets. It is the observation that people experience losses in a more severe way than an equivalent gain. In other words, humans prefer avoiding losses more than they like acquiring gains.

Traders also have an anchoring bias in that their sell orders are influenced by the price they paid for acquiring the asset. Loss aversion plays a significant role, in that it leads traders not to sell at a loss, even if they have a bearish sentiment towards the asset.

Although at first these psychological effects seems to only affect discretionary traders, it also is relevant for systematic algorithmic developers. Given the fact that any strategy is subject to a series of bad outcomes, a systematic trader might become conclude that his strategy lost its edge. Depending on their loss aversion, a trader could stop an algorithm even if the bad outcome was only caused by a series of unfavorable but random events.

Recommended platforms for paper trading stocks and cryptocurrencies

Paper Trading for Algorithmic Developers

Alpaca is not only an excellent broker to connect a real-life trading algorithm to, but also has one of the most reliable paper trading platforms available to developers. You can access financial data via their well-documented API and even use live data via their free Websockets. By sending orders to their endpoints, you can start simulating a trading strategy in under 1 hour. In fact I created an article that guides you step-by-step in doing so.

Paper Trading for Discretionary Traders

When it comes to simulating discretionary strategies, both Investopedia’s Simulator and Tradingview are viable options. Whereas Investopedia also serves as one of the most complete sources of information related to finance on the internet, TradingView is the go-to tool used by intraday traders that use charts and technical analysis.

No responses yet