The large fluctuations in international financial markets in recent decades are mainly a reflection of global economic crises. By becoming the variable most considered by investors to make their allocation decisions and causing a change in the structure of income on a global scale, the effects of investments in capital markets prevail over direct investment.

Traditional finance theories postulate a direct relationship between the financial sector and economic development. These theories have recently been expanded to indicate that there is a direct relationship between stock market performance and economic growth. The experimental evidence produced results that demonstrate a bidirectional interaction between both sectors.

The relationship between financial development and economic growth has been widely discussed. It is well identified that financial development is crucial for economic growth and vice versa. Various scholars, such as Schumpeter, have recognized this all-important relationship.

Having said this, let’s dive into the many ways in which financial markets are related to economic growth.

Table of Contents

Relationship between financial markets and economic growth

According to the authors Guzmán, Leyva, and Cárdenas, the relationship between the financial system and economic growth can be presented in two ways:

- The degree to which the development of the financial sector improves the allocation of resources between projects. This is due to the fact that developed markets promote better analysis of information, which allows choosing among the most profitable projects, thereby increasing the productivity of capital and economic growth.

- Financial markets improve the eligibility of companies through risk diversification. If the market matures, highly profitable investments can be financed, even if the projects are less liquid and riskier. This indicates that there is an integration between financial market capitalization and technology. Thus, the existence of a relationship between financial development and economic growth is based on the fact that the increase in market capitalization, which allows companies to easily access financial resources, translates into an increase in the productivity of all their factors, favoring thus economic growth.

So, can we be talking about a direct relationship between economic growth and financial markets? Let’s look at the charts.

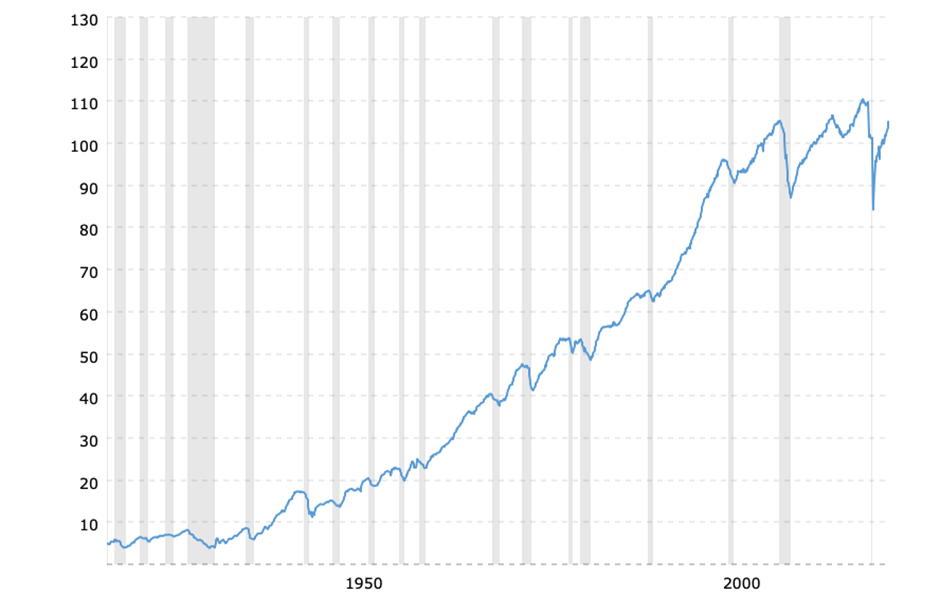

In the first chart, we can see how the financial market was affected by economic recessions in almost 90% of them.

The second graph presents the index of industrial production, which logically accompanied economic growth (and vice versa).

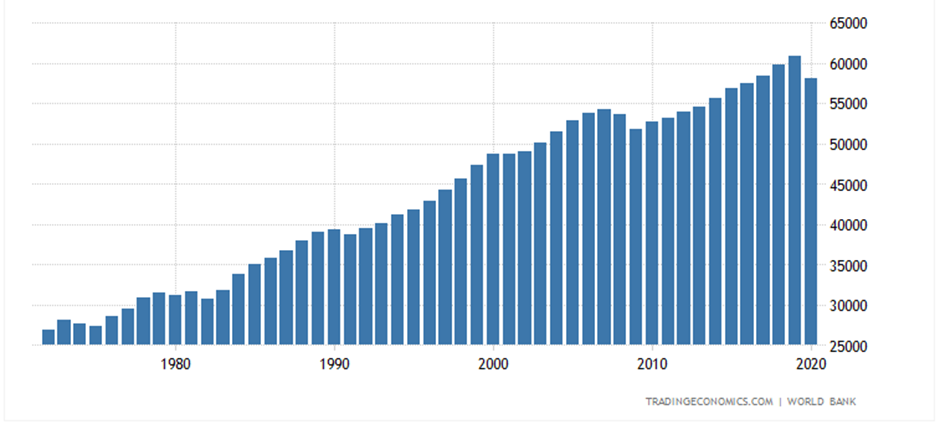

Finally, GDP Per Capita* shows how it also accompanies the growth of the financial markets.

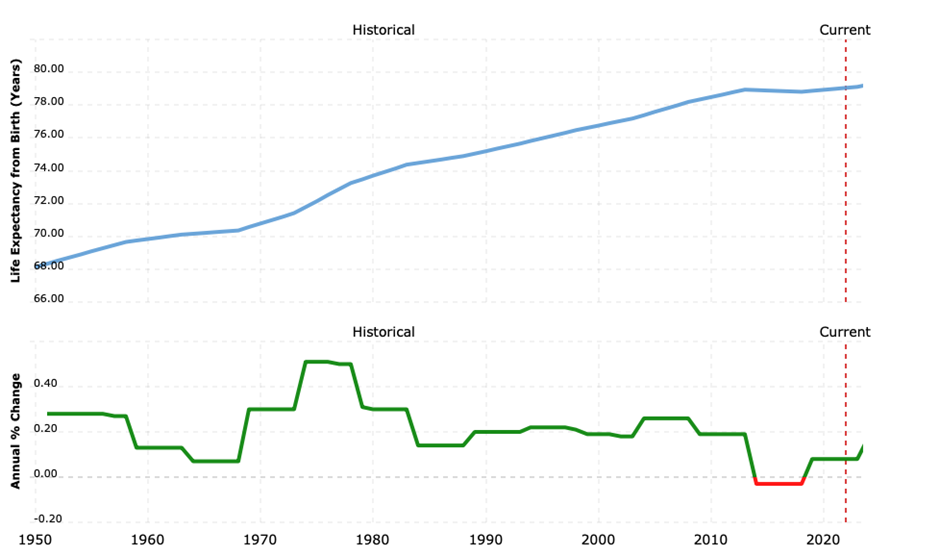

With economic growth, life expectancy also increases. In the most developed countries, aspects such as pharmaceutical spending, and health spending, among other things, stand out as determining factors; such as literacy and nutrition.

We must bear in mind that life expectancy is a very important indicator, which is used to analyze human behavior. Thus, life expectancy affects fertility, economic growth, and investment in human capital.

A high GDP per capita is related to high life expectancies.

*: Measures the sum of the gross value added of all resident producers in the economy plus any taxes on products (minus subsidies) not included in the production valuation, divided by the population of the middle of year

Advantages of Financial Markets for Economic Growth

Financial markets are essential for startups

Although most startups finance themselves via seed investors and venture capitalists during their first years of existence, the stock market serves a major role in the proliferation of these.

Seed investors and venture capitalists invest in a handful of startups under the assumption that a few of these will eventually have an initial public offering (IPO) down the road. In order for these investors to invest in a startup today, they require the existence of stock markets in order to sell their holdings, at least partially, roughly 10 years into the future.

Countries with less-developed stock markets also feature a less thriving startup scene. This is in part due to the absence of investors willing to allocate their resources to these risky endeavors due to the absence of a market that will allow them to turn their investments into liquid cash. As a consequence, stock markets are a necessary but not sufficient condition for startups to emerge and develop.

Financial Markets are essential for financing companies

In financial markets, funds are transferred from those who have surplus funds to those who need them. They allow college students to take out loans, families to take out mortgages, businesses to finance their growth, and governments to finance their deficits.

Individuals and companies that have excess funds are willing to supply them to the financial markets due to the expectation of a return on their investment. If they did not, these markets would not be able to transfer the funds to those who require them.

- Participants who receive more money than they spend are known as surplus units (or investors), which provide their net savings to the financial markets.

- Those that spend more money than they receive are called deficit units; they have access to funds from the financial markets in order to be able to spend more money than they generate.

Numerous individuals provide funds to the financial markets during some periods and have access to the funds in others. Financial markets allow economic units to intertemporally allocate their resources as they see fit.

Numerous deficit units, such as companies and government agencies, have access to funds from financial markets through the issuance of securities or titles, which are certificates that represent a credit to the issuer. Debt securities represent debt incurred by the issuer.

Equity securities represent the ownership interest in a company. Some companies may prefer to issue equity securities instead of debt securities when they need funds since they do not have the economic conditions to make the periodic interest payments that debt securities entail.

A key role of financial markets is to accommodate corporate financial activities. Financial markets serve as the mechanism by which companies (acting as deficit units) can obtain funds from investors (acting as surplus units).

In turn, equity capital markets facilitate the flow of funds from individual or institutional investors to corporations. Therefore, they allow them to finance their investments for new business initiatives or to expand the ones they already have.

When a company goes public, it issues equity capital on the primary market in exchange for cash. With this, its ownership structure changes, since the number of owners increases, and the capital structure of the company changes, because its equity investment increases, which allows it to pay off part of its debt and expand its operations.

The massive growth of the equity capital market has allowed many corporations to expand at a higher rate of growth, and investors to share in the profitability of operations.

Financial Markets improve liquidity

Investors prefer liquid securities, which means they can be easily converted to cash without high transaction costs.

If an exchange has a high volume of transactions, the price that a buyer offers for the share (bid) and the price that the seller is willing to accept (ask), tend to be similar. In other words, the buyer would not have to pay more to buy the shares and the seller can easily liquidate them. When the spread between the bid and ask prices (spread) widens, the market becomes more illiquid.

It is important to consider the time of day. Transactions that take place outside of regular trading hours tend to carry higher transaction costs since there are fewer parties in the market and, consequently, the liquidity of the market is lower.

Orders within the financial market are arranged within the so-called “order book“, which shows the buying parties at the highest price they want to buy the asset, and the selling parties at the lowest price they are willing to sell it. Every publicly traded asset has its own order book.

As investors load their orders according to their specifications, the order book is updated according to the following criteria:

- Price: buying orders are ordered in decreasing order (highest price first, a lowest price last), whereas selling orders are ordered in increasing order ( lowest price first, highest price last).

- Time: If two orders from the same side are quoted at the same price, the one that was first created will get priority. This follows the first-in-first-out (FIFO) methodology.*

What does it mean? That the boxes will be completed with the tips that have the best price. In other words, the cheapest ask offer and the most expensive ask offer. When the price of both parties agrees, the order is completed: the seller gets the money and the buyer the assets.

*: The price-time criteria is the most widely used across exchanges, but definitely not the only possible methodology.

Developed Financial Markets improve Transparency

If stock markets are efficient, stock prices will at any time reflect all available information (at least in theory). Stock prices adjust immediately, as investors try to take advantage of all the new information that is not yet substantiated.

Investors often overreact or underestimate information. This does not mean that markets are inefficient on aggregate unless the reaction is generalized and biased in the same direction. Investors who recognize this polarization will be able to earn abnormally high risk-adjusted returns.

The greater the efficiency of a market, the lower the transaction costs and the greater its liquidity. As previously mentioned, this translates into higher potential economic growth.

A brief sidenote on market efficiency

The efficiency of markets can be classified in three ways: weak efficiency, semi-strong efficiency, and strong efficiency.

- Weak-form efficiency suggests that security prices reflect all information related to transactions, such as historical movements in the price of securities and the volume of securities traded.

- Semi-strong form efficiency suggests that stock prices fully reflect all public information. The difference between public information and market-related information is that the former includes announcements made by companies, news, or economic events. Market-related information is a subset of public information.

- Strong efficiency suggests that stock prices fully reflect all information, including proprietary or confidential information. If the strong form efficiency holds, the semi-strong form efficiency will too. However, if insider information leads to abnormal returns, the efficiency might be presented in a semi-strong form, and not the efficiency in a strong form. It gives trusted people an unfair advantage over other investors.

Why is the secondary market important for economic growth?

Primary markets facilitate the issuance of new titles or securities. Secondary markets facilitate the exchange of existing titles, which allows the transfer of ownership of them.

For example, most types of debt securities have a secondary market, so investors who initially purchase them in the primary market do not have to hold them to maturity. Transactions in the primary market provide funds to the initial issuer of the securities; secondary market transactions do not.

An important characteristic of securities traded in secondary markets is liquidity, which is the degree to which the securities can be easily liquidated (sold) without losing value. Some titles have an active secondary market, which means that at any given time there are many buyers and sellers of the title. Investors prefer liquid securities so they can easily sell them whenever they want. If a security is illiquid, investors may not find a buyer in the secondary market and may have to sell it at a lower price to attract a buyer.

No responses yet